A Cash Equivalent Satisfies Which of the Following Criteria

A it is expected to be realised in or is intended for sale or consumption in the entitys normal operating cycle. According to PAS 1 an asset shall be classified as current when it satisfies any of the following criteria except a.

2

Where the normal operating cycle cannot be identified it is assumed to have a duration of 12 months.

. Any items falling within this definition are classified within the current assets category in the balance sheet. Cash and cash equivalents shall be classified as. B it is held primarily for the purpose of being traded.

Are more liquid than cash. An asset is a current asset if it satisfies any of the following criteria. D it is cash or a cash equivalent as defined by IAS7.

It is cash or a. It is expected to be realized within twelve months after the balance sheet date d. It is expected to be realized in or is intended for sale or consumption in the entitys normal operating cycle b.

An operating cycle is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. Include short-term investments purchased within 3 months of their maturity dates. It is expected to be settled in the entitys normal operating cycle.

It is held primarily for the purpose of being traded. An asset shall be classified as current when it satisfies any of the following criteria. It is cash or a cash equivalent.

According to PAS 1 an asset shall be classif ied as current when it satisfies any of t he follow ing. An item should satisfy the following criteria to qualify for cash equivalent. Of an asset liability income or expense and satisfies the following criteria.

It is cash or a cash equivalent which is unrestricted from being exchanged or used to settle a liability for at least twelve months after the balance sheet date. It is he ld prima rily for t he purpos e of bein g traded. A it is expected to be realised within the entitys normal operating cycle.

It is due to be settled within twelve months after the balance sheet date. Are readily convertible to a known cash amount. B it is held for the purpose of being traded.

C it is expected to be realised within twelve months after the reporting date. Cash and cash equivalents i Cash shall include cash balance chequesdrafts in hand and balances with banks in current accounts. Are more liquid than cash.

Are readily convertible to a known cash amount. To generate future cash flows. It is held primarily for the purpose of being traded.

The investment should be short term. 79 PPSAS 1 b. A liability shall be classified as current when it satisfies any of the following criteria.

Have a market value that is not sensitive to interest rate changes. Cheques drafts on hand. Be readily convertible to a known amount of cash.

Have a market value that is not sensitive to interest rate changes. Be close to its maturity so its market value is unaffected by interest rate changes. They should mature in less than three months.

The two primary criteria for classification as a cash equivalent are that an asset be readily convertible into a. A liability shall be classified as current when it satisfies any of the following. A liability shall be classified as current when it satisfies any of the following criteria.

Criteria exce pt. Cash and cash equivalents is a line item on the balance sheet stating the amount of all cash or other assets that are readily convertible into cash. The entity does not have an unconditional right to defer settlement of the liability for at least twelve months.

Companys normal operating cycle. B it is held primarily for the purpose of being traded. Cash equivalents meet all of the following criterla except Multiple Choice Readily convertible to a known cash amount Short-term Investments purchased within 3 months of their maturity dates.

It is cash or a cash equivalent as defined in PBE IPSAS 2 Cash Flow Statements unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date. Cash provided byused by. All other assets shall be classified as non-current.

What are some ways Cash Flows can help readers assess a financial statements. An asset that satisfies any of the following criteria. Cash flow information provides users of financial reports with a basis to assess the ability of the entity to generate cash and cash equivalents and the needs of the entity to utilise those cash flows.

AASB 107 sets out requirements for the presentation of the cash flow statement and related disclosures. It is expected to be realized within 12 months after the reporting period. Cash equivalents meet all of the following criteria except.

Operating cy cle. A it is probable ie more likely than not that any future economic benefit associated with. Measurement of Cash Flows.

B it is held primarily for the purpose of being traded. An asset shall be classified as current when it satisfies any of the following criteria choose the incorrect one. It is exp ected t o be realized in or is intended for s ale or consumption i n the entitys normal.

Sufficiently close to maturity so that market value is unaffected by interest rate changes. Cash equivalents meet all of the following criteria except. It is cash or a cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date.

All other assets shall be classified as non-current. Cash and cash equivalents. Ii Cash equivalents shall include short-term highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value.

More liquid than cash. Short-term highly liquid investments. O Have a market value that is not sensitive to Interest rate changes.

Include short-term investments purchased within 3 months of their maturity dates. Readily convertible into cash. An asset shall be classified as current when it satisfies any one of the following criteria.

It is expected to be realized in or is intended for sale or consumption in the entitys normal operating cycle. Earmarked balances with banks for example for unpaid dividend shall be separately stated. A it is expected to be realized in or is intended for sale or consumption in the companys normal operating cycle.

An asset shall be classified as current when it satisfies any of the following criteria a it is expected to be realised in or is intended for sale or consumption in the. It is held primarily for the purpose of being traded c. C it is expected to be realised within twelve months after the reporting date.

A current asset is an asset that satisfies any of the following criteria. C it is expected to be realised within 12 months after the reporting period. Common examples of cash equivalents include commercial paper treasury bills short term government bonds marketable securities and money market holdings.

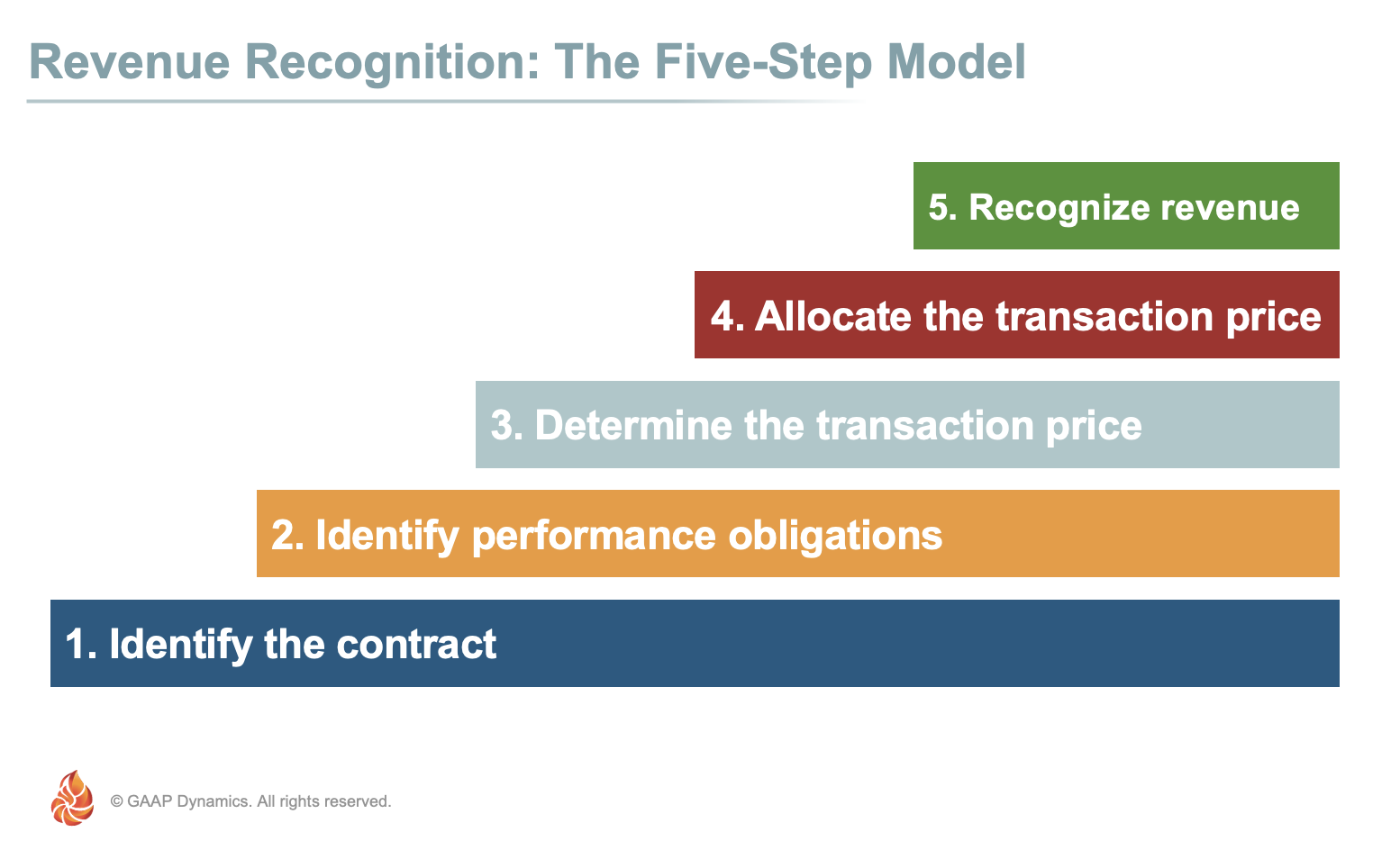

Revenue Recognition Gaap Dynamics

Ocr Maths On Twitter Math Factors And Multiples Math 5

Revenue Recognition Gaap Dynamics

Revenue Recognition Gaap Dynamics

Introduction There Is No Statutory Obligation Upon Sole Proprietorship Or Partnership Firm To Prepare Final Accounts But Companies Have A Statutory Ppt Download

Framework For Financial Statement In Accordance With Ind As Purpose Scope Objective

You Can T Buy Antibiotics Over The Counter Can You Yes You Can

Large Containers For Holding Storage Water Legend Large 300 Liter Download Scientific Diagram

The Role Of Customers In Marketing Introduction To Business Deprecated

2

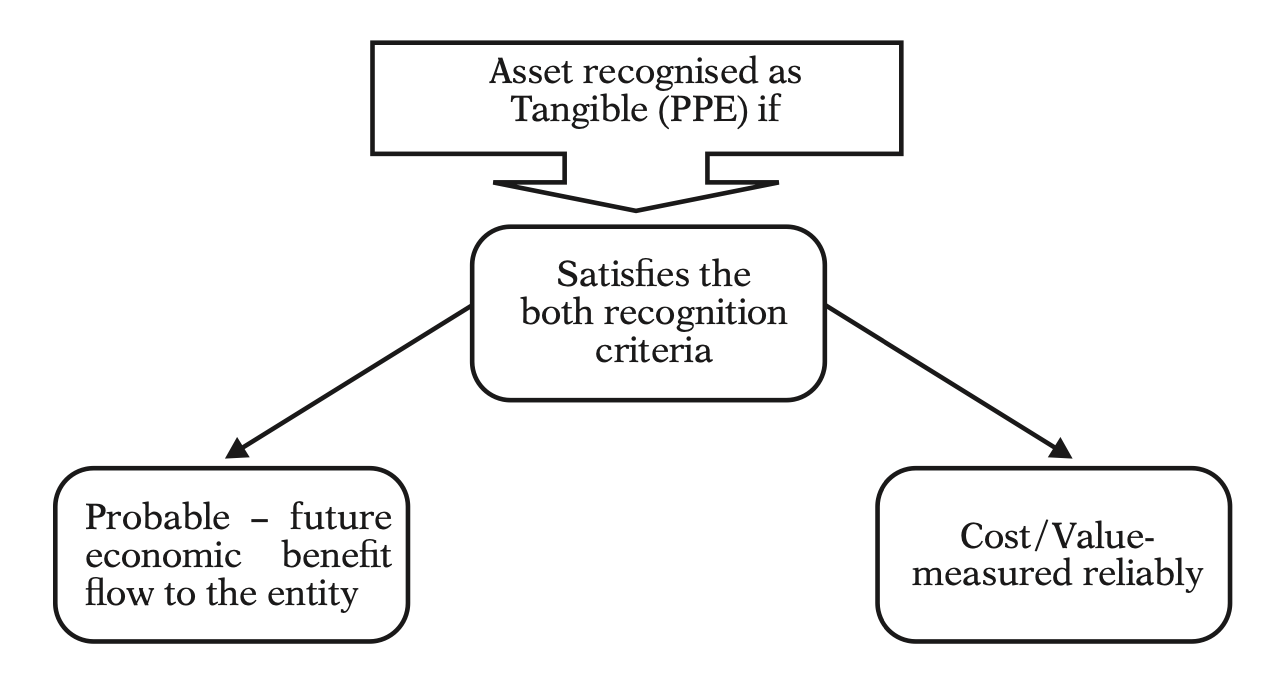

Ind As 16 Property Plant And Equipment With Illustrations Flow Charts Taxmann Blog

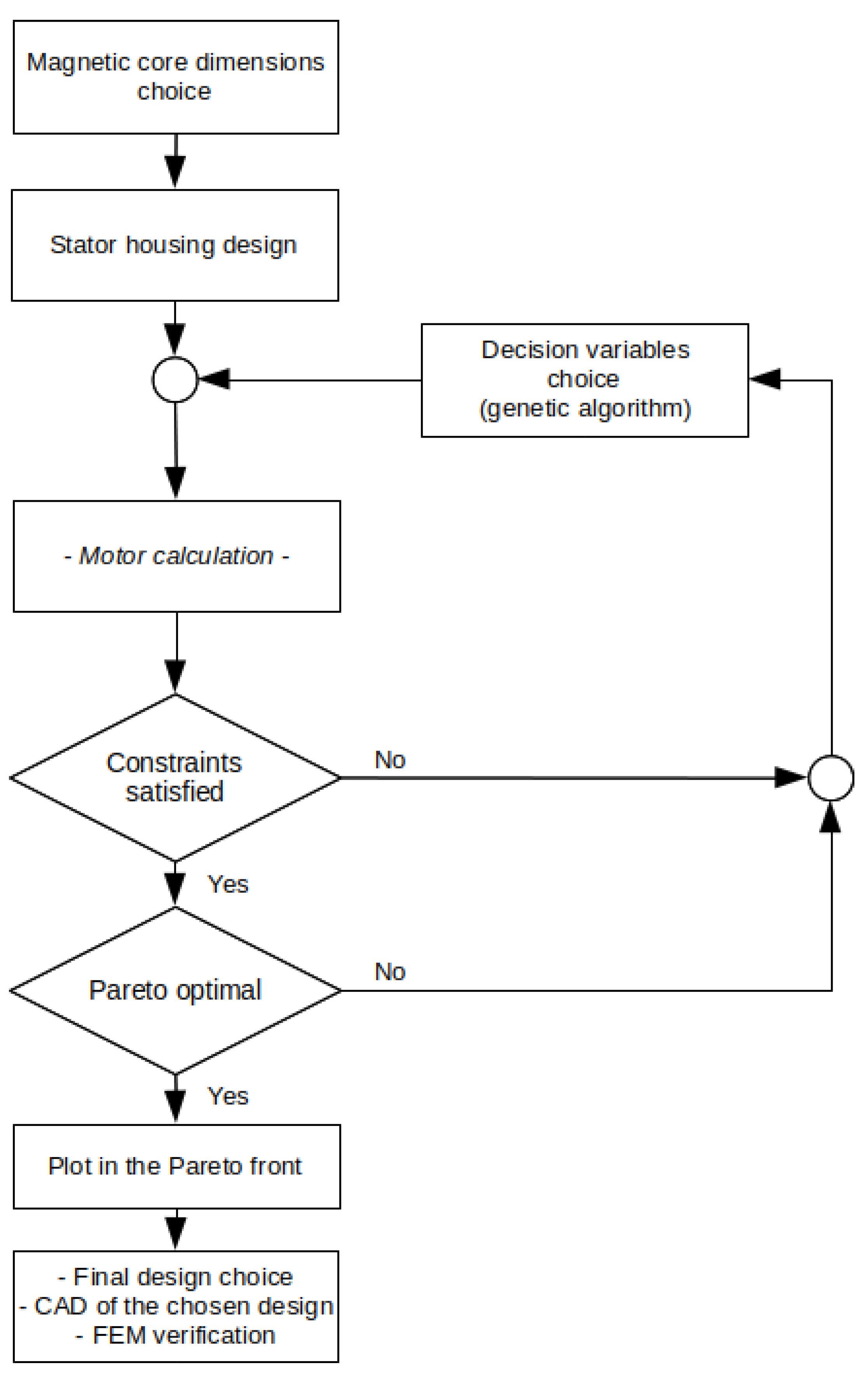

Energies Free Full Text Analytical Optimal Design Of A Two Phase Axial Gap Transverse Flux Motor Html

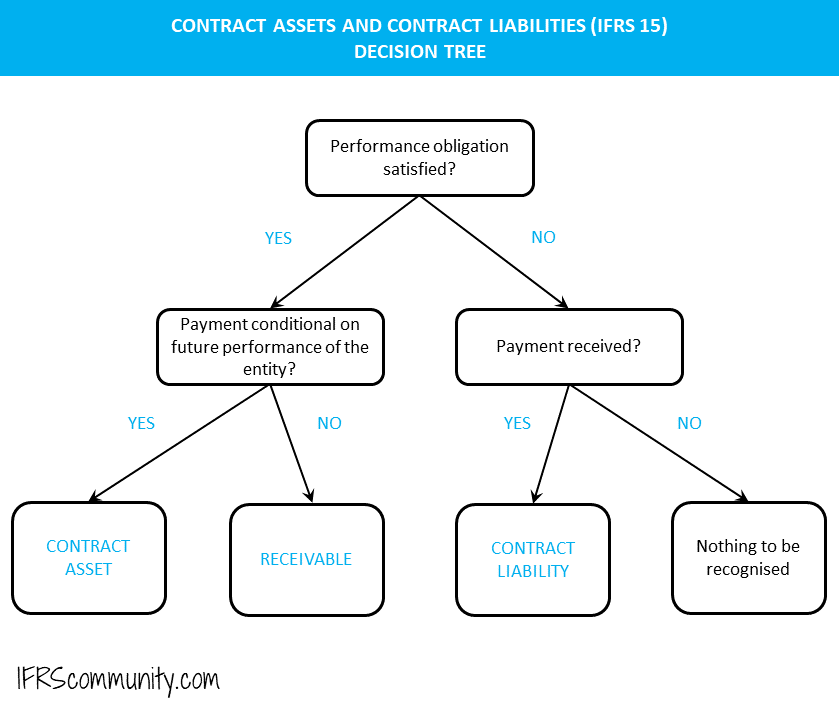

Contract Assets And Contract Liabilities Ifrs 15 Ifrscommunity Com

2

Capital Lease Criteria Top 4 Step By Step Examples With Explanation

A Firefly Algorithm Modified Support Vector Machine For The Credit Risk Assessment Of Supply Chain Finance Sciencedirect

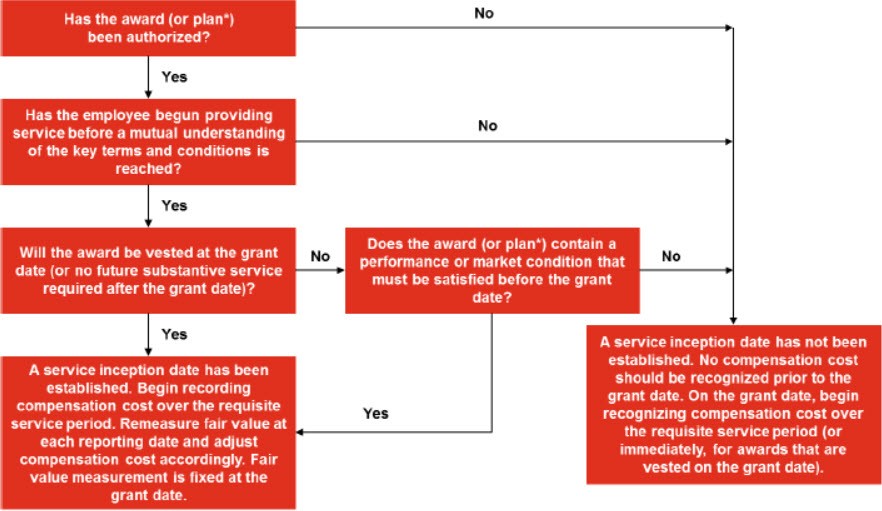

2 6 Grant Date Requisite Service Period And Expense Attribution

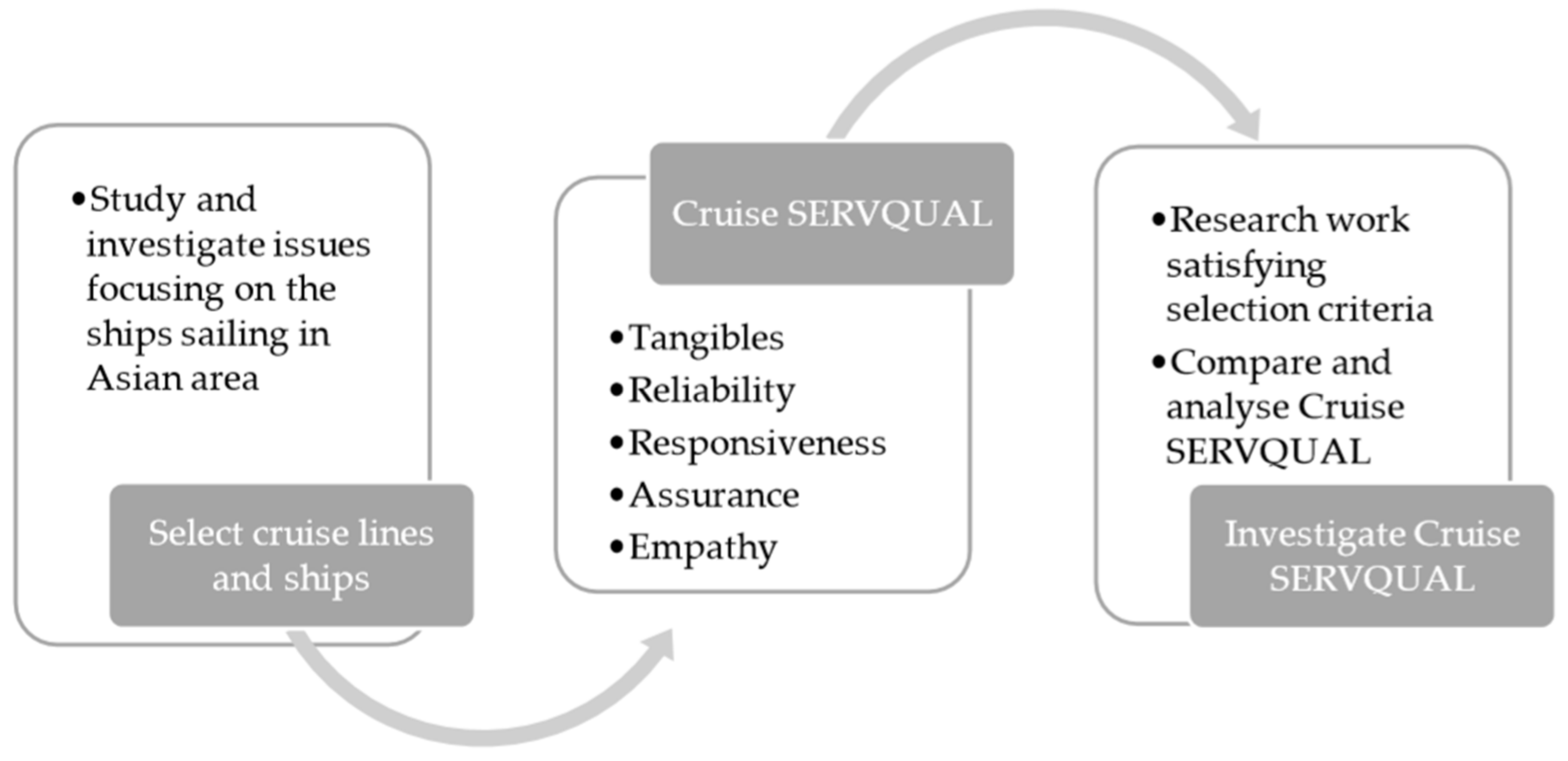

Sustainability Free Full Text A Qualitative Review Of Cruise Service Quality Case Studies From Asia Html

Revenue Recognition Gaap Dynamics

Comments

Post a Comment